Bitcoin

(unit of BTC) is now most successful and controversial virtual money which is

issued in 2009 by a pseudonymous developer named Satoshi Nakamoto.

As of March 2013, Bitcoin with a valued of 300 million

US dollars is

in circulation. [L5]

Bitcoin

can be used both for real and virtual goods. The scheme maintains a database

that lists

product and service providers which currently accept Bitcoins[L1]

These products and services range from internet services and

online products to material goods (e.g. clothing and accessories, electronics,

books, etc.), professional or travel/tourism services.[L1] A lot of online enterprises

such as WordPress, Mega, Reddit have accepted Bitcoin as a payment currency.

Bitcoins

are issued under certain rules and has a declining issuance rate which will be

reduced to 0 by 2040. And by that time, the total amount of Bitcoins will reach

21,000,000 BTC(10,500,000BTC at the very beginning). As there is not a central

management regulation, security of the system is ensured by its special rule

which stated that the new “gold” will be issued to those (miners) who help

calculate and validate the effectiveness of transactions. The calculation

consumed certain the resource of CPU as well as a huge amount of electricity

which can be seen as the value bases for the currency. In order to make the

money enough for trade, Bitcoin is divisible to eight decimal places.

Let’s

see some examples for the innovation of Bitcoins in retail payment.

Like

Wal-Mart purchased Card, we now have Bitbills(http://bitbills.com) which is a

kind of prepaid card storing Bitcoins to transact in real life stores without

internet connection. Users can either

exchange the cards at face value (for instance at a retailer) or redeem the

funds and spend them in the Bitcoin network.[L2] According to the creator of

this innovation, since their launch on 9 May 2011, the demand for Bitbills has

been substantial. [L2]

Another

important innovation related with retailing is a Bitcoin point of sale system (Casascius Bitcoin POS system ,https://en.bitcoin.it/wiki/Casascius_Bitcoin_POS_system)

developed in Oct, 2011.

Its main function is to

enable retailers to accept Bitcoins at the point of sale[L4].

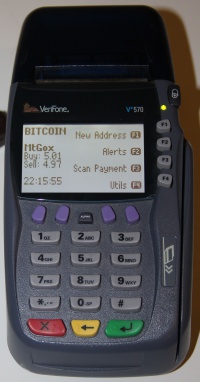

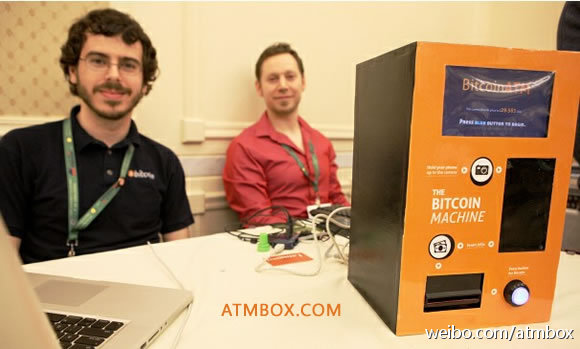

The most recent

inspiring innovation is a dollar-converting anonymous Bitcoin ATM invented by Zach

Harvey, right, and Matt Whitlock, who wished to sell them to bars, restaurant

and other retail places.[L5] Every ATM is

sold at 1000-1500 Dollars, considering the fact that shops like Cups and Cakes

Bakery in San Francisco and PizzaForCoins are all following the suit. We think

this ATM might be a big success in business. Just as the creator Harvey said:

“It’s so simple that I am just putting in a dollar, before they really know what's going on, their

phone tells them, 'you have Bitcoin’”

There

are many risks concerned with virtual money, including safety (Hacker), value

fluctuation (only exchange value, no deposit value), money laundering, policy

risk (legal status) and so on. All the problem happened in real money may

happen in virtual money.

However

there are also a lot of advantages in it. “The technology represents an easy

way to transfer funds across national borders, a process that currently can be

slow and cumbersome with wire transfers. Bitcoin is less risky for online

sellers than accepting credit cards. While not truly anonymous,

it can be relatively private -- and is far more difficult for the U.S. or other

governments to trace.”[L5]

And

two strong demands coming out of economic development are the most important

factors that make us optimistic on the future of Virtual Money.

Firstly,

the need of a unified currency is more and more obvious in a more and more

globalised economic environment. This is an irreversible process caused by

globalisation. The implementation of

Euro Scheme is a proof for the convergence trend of currency. And Virtual Money

with its feature beyond geographical limitation and redundant regulation

organizations can be a good model for a new Global Currency.

Second,

Technology such as RFID makes it possible for human beings to connect and trade

wirelessly through a global network. This significantly reduced the cost of

transaction, and makes virtual money a currency with strong vitality in a more

and more virtualised human society.

Although

it’s not likely those virtual money schemes existed today can long survive,

even the most successful Bitcoins, due to the political risk and the fact that

government is still the most significant power to make change. They can be

taken as experiments and drives for the emergence of a global based currency.

We can

conclude that with the development of RFID technology and M2M network, it is

possible for Bitcoin to become a drive to push for the birth of a new

governments involved globally unified virtual currency.

Bibliography(L):

1. Virtual

Currency Scheme, Oct 2012, by European Central Bank

2. BIS

(2012), “Innovations in retail payments”, Report of the Working Group on

Innovations in

Retail Payments, May.

4. Casascius Bitcoin POS system, Wikipedia

5. Need Bitcoins? This ATM takes dollars and

funds your account 23 Feb, 2013, by Declan McCullagh

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.